us japan tax treaty dividend withholding rate

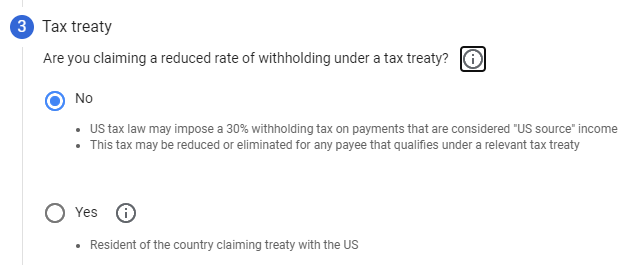

The tax is thus withheld or deducted from the income due to the recipient. These treaty tables provide a summary of many types of income that may be exempt or subject to a reduced rate of tax.

General Information On The Brazilian Tax System Bpc Partners

Amounts subject to withholding tax under chapter 3 generally fixed and determinable annual or periodic income may be exempt by reason of a treaty or subject to a reduced rate of tax.

. In the absence of a treaty Canada imposes a maximum WHT rate of 25 on dividends interest and royalties. Tax resident is entitled to the listed rate of tax from a foreign treaty country although generally the treaty rates of tax are the same. Normally the country of source would grant full or partial tax exemption or impose a reduced dividend withholding tax rate.

0 or 275 0 0 or 20. 0 0 0 Note that a rate of 49 applies in the case of interest and certain dividends where a Tax File Number is not quoted to the payer. 0 or 275 0 or 25 or 275 0.

The country in which the company paying the dividend is resident has the right to tax the dividend income. Tax withholding also known as tax retention Pay-as-You-Go Pay-as-You-Earn or a Prélèvement à la source is income tax paid to the government by the payer of the income rather than by the recipient of the income. Interest ccc Dividends Pensions and Annuities Income Code Number 1 6 7 15 Name Code Paid by US.

A zero rate of tax may apply in certain cases. In most jurisdictions tax withholding applies to employment income. Obligors General Treaty.

The treaty has been signed but is not yet in force. This table should not be relied on to determine whether a US. 30 10 30 Note there are certain exemptions that may apply Austria Last reviewed 11 January 2022 Resident.

Dividend income may be taxed in the recipients country of residence and that the country of source ie. The lower lowest two for Vietnam rate applies if the beneficial owner of the dividend is a company that ownscontrols a specified.

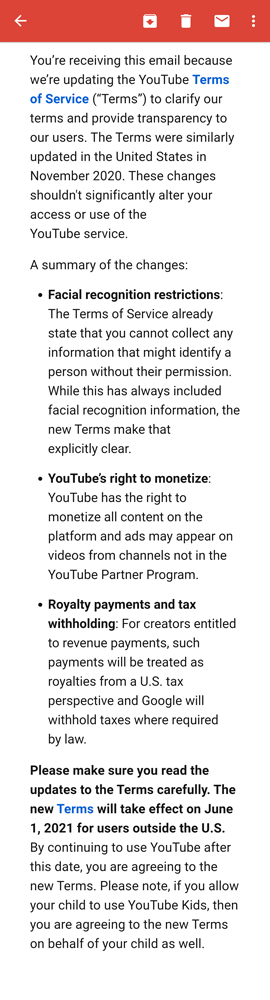

Youtube To Introduce Tax For Youtubers Outside U S Starting From June 2021 Tehnoblog Org

General Information On The Brazilian Tax System Bpc Partners

Possible Implications Of Integrating The Corporate And Individual Income Taxes In The United States In Imf Working Papers Volume 1990 Issue 066 1990

Japan And Spain Update Their Double Taxation Treaty No Withholding On Dividends Interest And Royalties Carlos Garcia Olias Santiago Tortola

Youtube To Introduce Tax For Youtubers Outside U S Starting From June 2021 Tehnoblog Org

Japan And Spain Update Their Double Taxation Treaty No Withholding On Dividends Interest And Royalties Carlos Garcia Olias Santiago Tortola

Status Of Russia S Initiative On Amending Its International Tax Treaties To Increase Withholding Tax Rate On Dividends And Interest To 15 Percent Deloitto China

Annex A Examples Tax Challenges Arising From Digitalisation Report On Pillar Two Blueprint Inclusive Framework On Beps Oecd Ilibrary

Global Corporate And Withholding Tax Rates Tax Deloitte

Possible Implications Of Integrating The Corporate And Individual Income Taxes In The United States In Imf Working Papers Volume 1990 Issue 066 1990

Guide To Taxes On Dividends Intelligent Income By Simply Safe Dividends

Youtube To Introduce Tax For Youtubers Outside U S Starting From June 2021 Tehnoblog Org

Japan And Spain Update Their Double Taxation Treaty No Withholding On Dividends Interest And Royalties Carlos Garcia Olias Santiago Tortola

Youtube To Introduce Tax For Youtubers Outside U S Starting From June 2021 Tehnoblog Org

Status Of Russia S Initiative On Amending Its International Tax Treaties To Increase Withholding Tax Rate On Dividends And Interest To 15 Percent Deloitto China

Youtube To Introduce Tax For Youtubers Outside U S Starting From June 2021 Tehnoblog Org

Possible Implications Of Integrating The Corporate And Individual Income Taxes In The United States In Imf Working Papers Volume 1990 Issue 066 1990

Guide To Taxes On Dividends Intelligent Income By Simply Safe Dividends

Annex A Examples Tax Challenges Arising From Digitalisation Report On Pillar Two Blueprint Inclusive Framework On Beps Oecd Ilibrary